Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Mortgage Rates Are Unpredictable—Here’s What Homebuyers Can Still Control

Mortgage Rates Are Unpredictable—Here’s What Homebuyers Can Still Control

Introduction

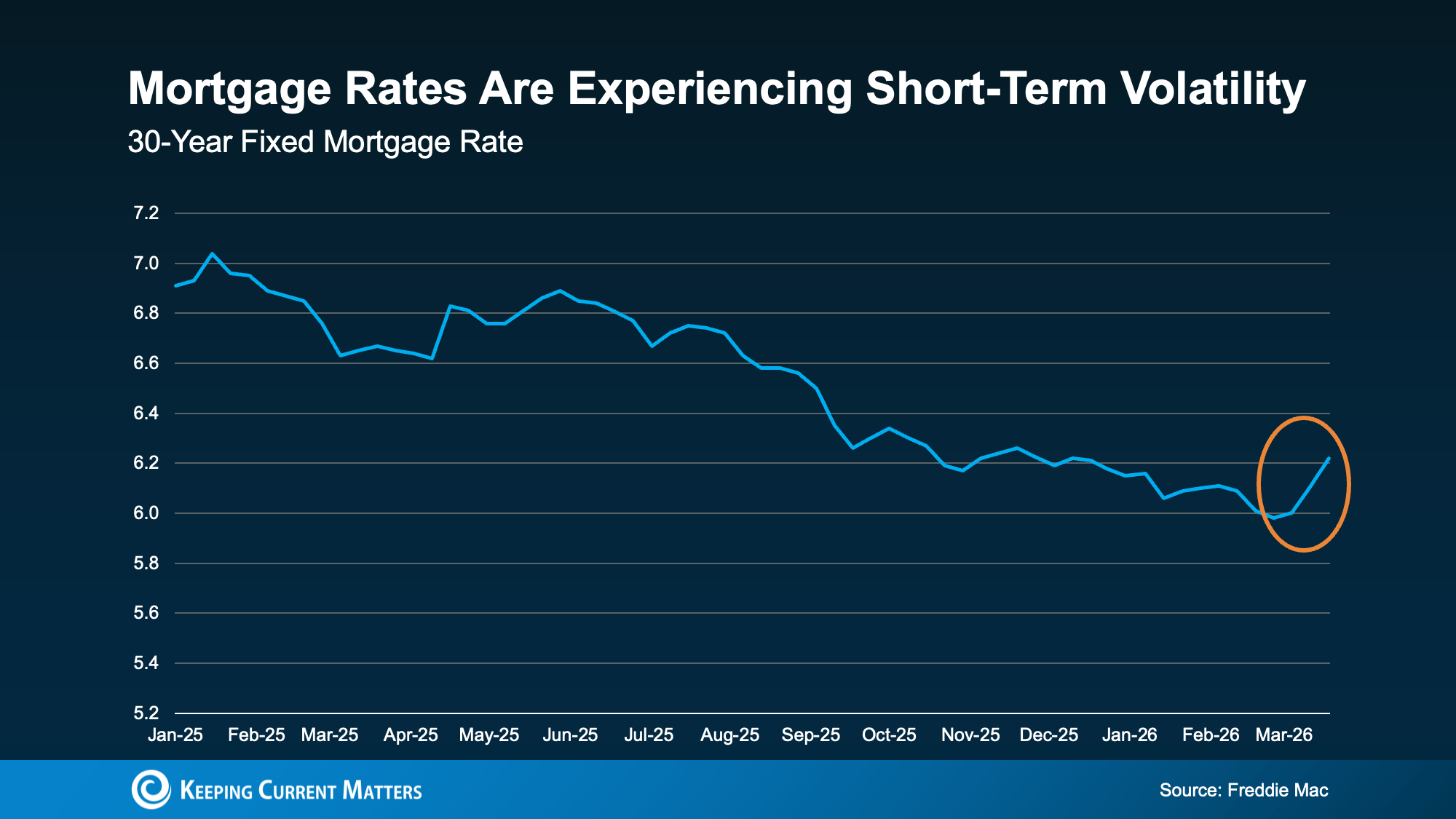

If you’ve been thinking about buying a home, you’ve probably noticed one thing: mortgage rates have been anything but steady. One week they dip, the next they climb—and that uncertainty can make it difficult to know when to make your move.

While no one can predict exactly where rates are headed, that doesn’t mean you’re powerless. In fact, there are several key factors within your control that can directly influence the rate you secure—and ultimately, how much you pay over time.

Let’s break down what’s really happening with mortgage rates and, more importantly, how you can position yourself for the best possible outcome.

Why Mortgage Rates Keep Fluctuating

Mortgage rates don’t move randomly—they react to larger economic forces. Inflation trends, global events, and financial market shifts all play a role in how lenders adjust borrowing costs.

Even after periods of stability or gradual decline, it’s completely normal to see short-term increases. These fluctuations often happen during times of economic uncertainty, and they can change quickly.

The key takeaway? Trying to “time” the perfect rate is rarely a winning strategy. Instead, successful buyers focus on what they can control—and act when they’re financially ready.

What You Can Control as a Homebuyer

While the market may be unpredictable, your personal financial profile plays a major role in the rate you’re offered. Here are three areas where your decisions can make a meaningful difference:

1. Your Credit Profile Matters More Than You Think

Your credit score is one of the most influential factors in determining your mortgage rate. Lenders use it to assess risk, and even small improvements can translate into better loan terms.

Why it matters:

-

Higher credit scores typically unlock lower interest rates

-

Lower rates mean reduced monthly payments

-

Over time, this can save you thousands of dollars

What you can do:

-

Pay down outstanding balances

-

Avoid opening new lines of credit before applying

-

Check your credit report for errors

If you’re unsure where you stand, a trusted loan officer can help you understand your score and identify ways to strengthen it.

2. The Loan Program You Choose Impacts Your Rate

Not all home loans are created equal. Different loan types come with varying requirements, benefits, and interest rate structures.

Some of the most common options include:

-

Conventional loans

-

FHA loans

-

VA loans

-

USDA loans

Each program is designed for different financial situations, and the rate you receive can vary significantly depending on which one you choose.

Pro tip: Don’t settle for the first option you’re offered. Comparing loan programs—and even multiple lenders—can reveal better opportunities.

3. Your Loan Term Shapes Your Long-Term Costs

The length of your mortgage also plays a major role in your rate and overall financial picture.

Typical loan terms include:

-

30-year loans (lower monthly payments, higher total interest)

-

15-year loans (higher monthly payments, lower overall interest)

What to consider:

-

Your monthly budget

-

Your long-term financial goals

-

How much interest you’re comfortable paying over time

Choosing the right term isn’t just about affordability today—it’s about building a strategy that works for your future.

Stop Waiting—Start Strategizing

It’s easy to feel stuck when rates are unpredictable. But waiting for the “perfect” moment can sometimes mean missing out on the right home altogether.

Instead of focusing on market timing, shift your attention to preparation:

-

Strengthen your financial profile

-

Explore your loan options

-

Partner with experienced professionals

That’s how you move forward with confidence—regardless of where rates go next.

Bottom Line: Focus on What You Can Control

Mortgage rates will continue to change—that’s a given. But your approach as a buyer can have a direct impact on the rate you secure and the success of your home purchase.

If you’re considering buying, the smartest move is to build the right strategy and surround yourself with the right team.

Ready to Take the Next Step?

Whether you’re just starting to explore your options or you’re ready to begin the home search, having the right guidance makes all the difference.

Connect with CENTURY 21 Jordan-Link & Company today to get expert insight, trusted lender referrals, and a clear plan tailored to your goals.

Hispanic Homebuyers Driving U.S. Housing Growth in 2025

Hispanic Homebuyers Are Driving U.S. Housing Growth in 2025

A Record-Breaking Shift in the American Housing Market

In 2025, Hispanic homebuyers are not just participating in the U.S. housing market—they are driving it.

According to data from the National Association of Hispanic Real Estate Professionals (NAHREP), Hispanic households added a net gain of 441,000 new homeowners in 2025, the largest increase ever recorded. At a time when overall homeownership growth is slowing, this demographic has become the primary engine sustaining the market.

In fact, without Hispanic buyers, the U.S. housing market would have experienced a net decline in homeownership.

This trend signals a profound shift in who the future homeowner is—and where real estate professionals should be focusing their attention.

The Demographic Power Behind the Growth

The Hispanic population is uniquely positioned to shape the future of housing in the United States.

- The median age of Hispanics is approximately 31 years old, significantly younger than the overall U.S. population

- Hispanic households accounted for the majority of new household formations in 2025

- Total Hispanic homeownership has now surpassed 10 million households

This is not a temporary spike. It is a long-term demographic wave.

Industry projections suggest that Hispanic buyers could account for up to 70% of new homeowners over the next two decades.

For real estate professionals, this represents one of the most important shifts in modern housing history.

Why Hispanic Buyers Are Leading the Market

Several factors explain why Hispanic households are driving homeownership growth:

1. Strong Household Formation

Hispanic families are forming households at a faster rate than other demographic groups, creating sustained demand for housing.

2. First-Time Buyer Momentum

A large portion of Hispanic buyers are entering the market for the first time, contributing to net growth rather than replacement transactions.

3. Cultural Emphasis on Homeownership

Homeownership is often viewed as a key milestone for financial stability and generational wealth within Hispanic communities.

4. Multigenerational Buying Power

Many Hispanic households pool resources across family members, allowing them to overcome affordability barriers that might limit other buyers.

The Challenges Slowing Momentum

Despite strong demand, several major headwinds are limiting the full potential of Hispanic homeownership growth.

Housing Inventory Shortage

The lack of available homes remains the single biggest constraint. Demand is outpacing supply, making it difficult for motivated buyers to find suitable properties.

Credit Access Barriers

Many Hispanic buyers face challenges with traditional credit systems, including thin credit files or reliance on nontraditional financial histories.

Modernizing underwriting standards and expanding alternative credit models could unlock significant additional demand.

Affordability Pressures

Rising home prices and elevated interest rates continue to put pressure on first-time buyers, particularly those entering the market without existing equity.

Policy and Immigration Concerns

Immigration-related uncertainty can influence buyer confidence, while labor shortages in construction—often tied to immigration policy—further constrain housing supply.

What This Means for Real Estate Professionals

The implications of this shift are clear: agents and brokers who adapt to serve Hispanic buyers will be better positioned for long-term success.

Build Bilingual and Culturally Relevant Marketing

Effective communication goes beyond translation. It requires culturally relevant messaging that resonates with values such as family, stability, and legacy.

Focus on Education-Based Content

Many first-time buyers benefit from guidance around financing, credit, and the homebuying process. Educational content builds trust and positions agents as advisors.

Embrace Community-Centered Strategies

Relationships and referrals play a significant role in Hispanic communities. Local engagement and community presence are key drivers of business growth.

Understand Multigenerational Dynamics

Purchasing decisions may involve multiple family members. Agents who recognize and accommodate this dynamic can better serve their clients.

The Future of U.S. Homeownership

The data is clear: Hispanic homebuyers are not just influencing the market—they are defining its future.

As this young, fast-growing demographic enters peak homebuying years, their impact will only continue to expand.

For industry professionals, the opportunity is significant. Those who invest in understanding and serving this audience today will be positioned to lead tomorrow’s housing market.

Sources

- National Association of Hispanic Real Estate Professionals (NAHREP)

- HousingWire

Unlocking Your Home’s Potential: How to Use Equity to Fund Smart Renovations

Your Dream Upgrades Might Already Be Within Reach

That kitchen you’ve been picturing with updated finishes…

The bathroom that could use a modern refresh…

The backyard you’ve been meaning to turn into a true outdoor retreat…

What if the funds to make those upgrades happen are already available to you?

Many homeowners are tapping into one powerful resource to transform their living spaces—home equity. Instead of putting renovations off year after year, they’re strategically reinvesting in their homes while increasing long-term value.

What Is Home Equity and Why Does It Matter?

Home equity represents the gap between your property’s current market value and the remaining balance on your mortgage.

Over time, as property values rise and loan balances decrease, equity grows—often significantly. In today’s market, many homeowners have built substantial equity, creating an opportunity to reinvest in their property without relying solely on savings.

This financial flexibility is one of the biggest advantages of long-term homeownership—and it can be a game changer when it comes to upgrades.

Why Homeowners Are Using Equity Right Now

Home improvement is one of the most common reasons homeowners access their equity—and for good reason.

Here’s how equity is commonly being used:

- Home renovations and upgrades (most popular use)

- Debt consolidation or paying off high-interest balances

- Investing in additional real estate opportunities

Among these, improvements that enhance comfort, functionality, and resale value are leading the way.

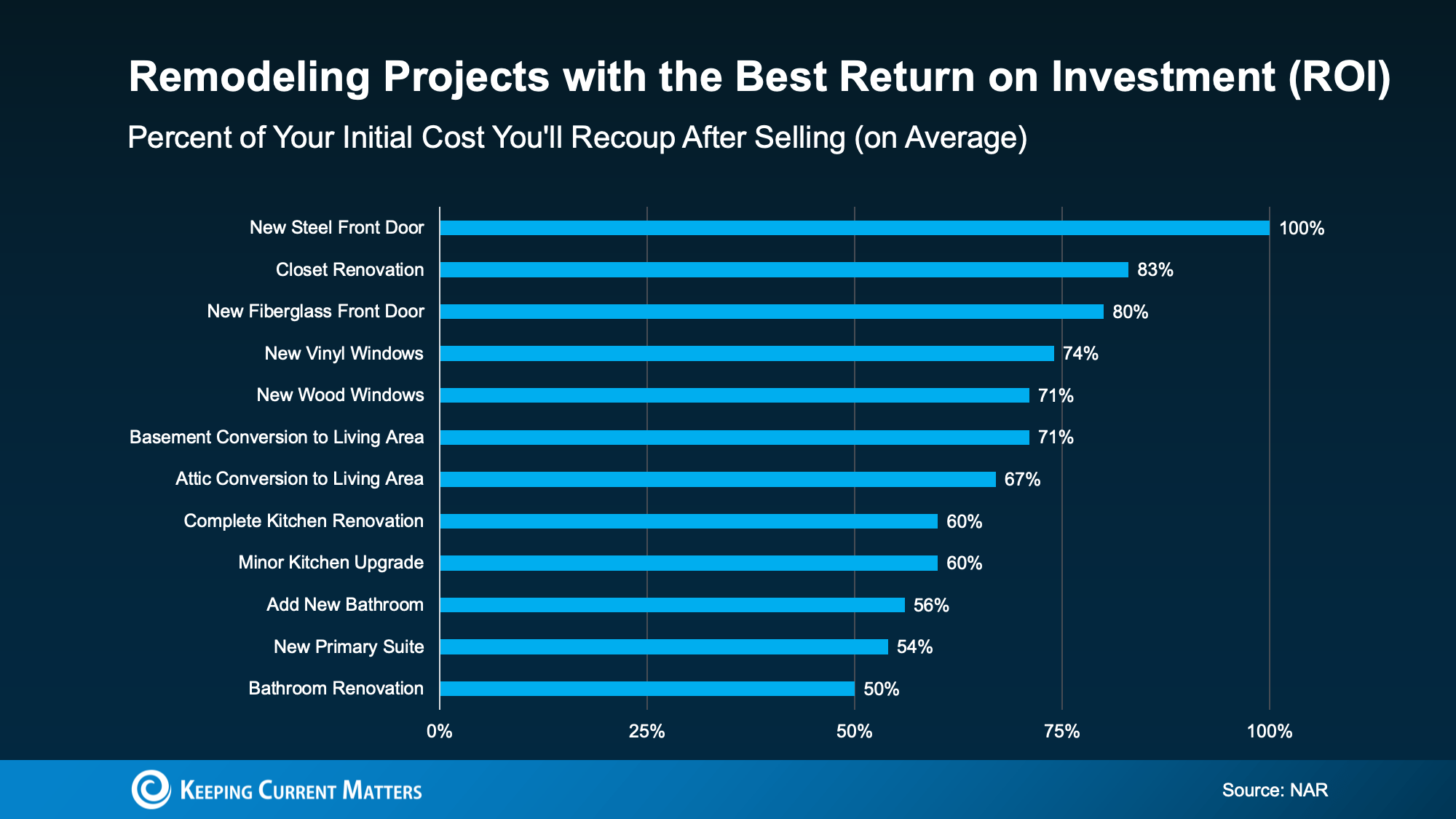

Not All Renovations Are Equal: Focus on ROI

Before diving into any project, it’s important to think beyond aesthetics. The goal isn’t just to upgrade—it’s to add value.

Some renovations consistently deliver stronger returns than others, including:

- Kitchen upgrades that modernize layout and finishes

- Bathroom remodels that improve functionality and appeal

- Entryway enhancements like a new front door or improved curb appeal

- Minor cosmetic updates with high visual impact

While large-scale remodels can be exciting, smaller, strategic updates can sometimes offer a better return relative to cost.

Why Working with a Real Estate Agent Matters

Choosing the right project isn’t always straightforward—and this is where a local real estate expert becomes invaluable.

An experienced agent can help you:

- Identify which upgrades buyers in your area actually want

- Avoid over-improving beyond neighborhood standards

- Prioritize projects that maximize resale value

- Align your renovation plans with current market trends

At CENTURY 21 Jordan-Link & Company, we guide homeowners through these decisions every day—helping you invest confidently and strategically.

Smart Planning: Key Considerations Before Using Equity

Just because you can access your equity doesn’t always mean you should—at least not without a plan.

Before moving forward, consider:

- Your long-term goals: Are you selling soon or staying put?

- Loan-to-value (LTV) impact: How borrowing affects your financial position

- Project scope vs. return: Will the upgrade pay off in your market?

- Professional guidance: Input from both a real estate agent and financial advisor

A well-informed approach ensures your investment works for you now and in the future.

Where to Start: Turn Ideas into a Strategic Plan

If you’ve been thinking about upgrading your home, the next step isn’t calling a contractor—it’s getting clarity.

Start by:

- Listing the improvements you’re considering

- Evaluating which ones add the most value

- Talking with a local real estate expert

- Exploring financing options if needed

The goal is simple: maximize impact while minimizing unnecessary spending.

Bottom Line: Invest in Your Home with Confidence

The right improvements can elevate your daily living experience while strengthening your home’s long-term value. And with the amount of equity many homeowners have today, those upgrades may be more achievable than expected.

The key is making smart, informed decisions about where and how to invest.

Ready to Make a Move? Let’s Talk

Thinking about upgrading your home but not sure where to start?

Connect with a local expert at CENTURY 21 Jordan-Link & Company to discuss your goals, evaluate your options, and create a plan that makes sense for your property and your future.

Your next step starts with a simple conversation.

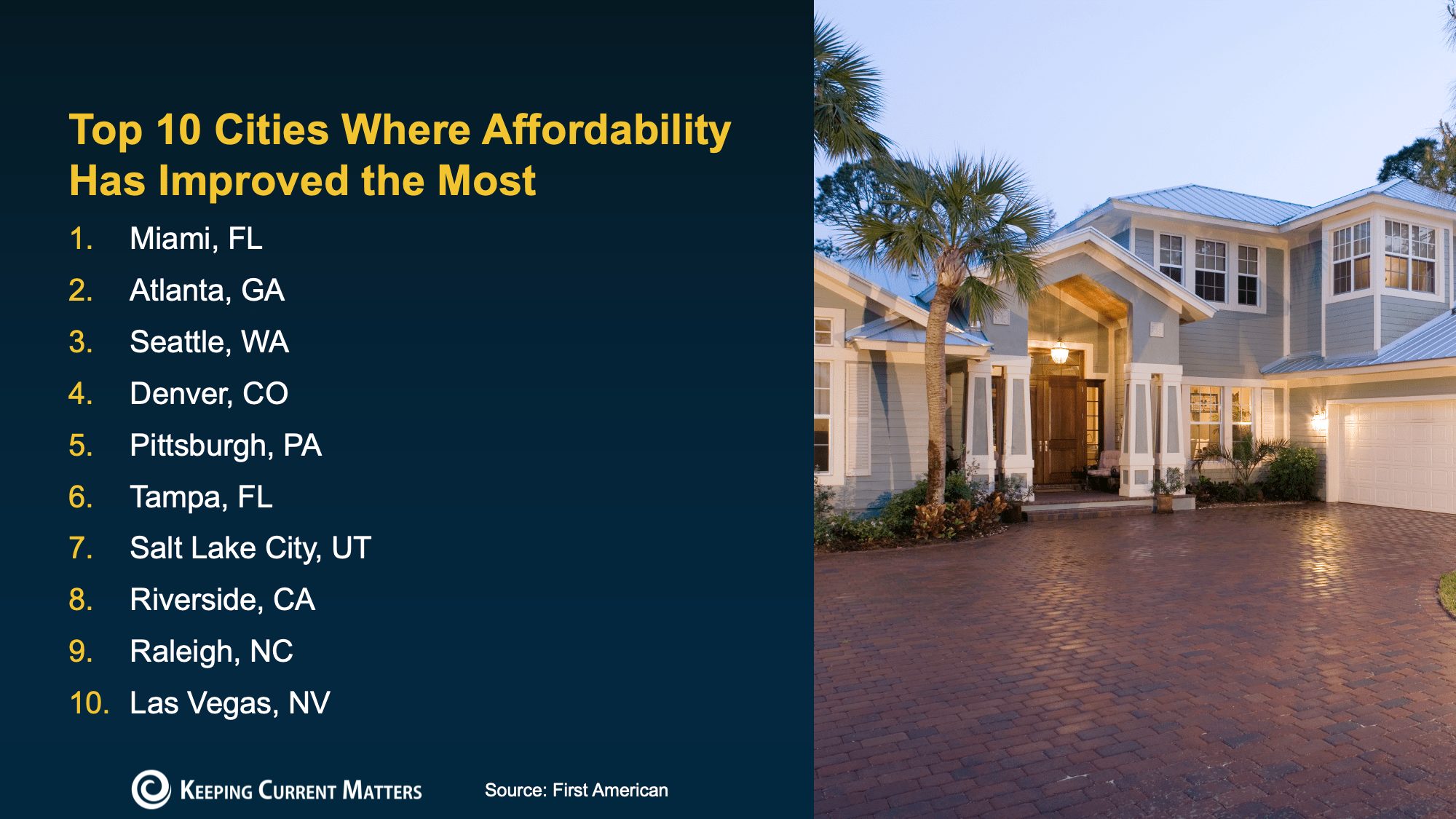

Housing Affordability Is Improving in All 50 States: What Buyers Need To Know in 2026

⚡ AI Answer Summary

Housing affordability has improved in all 50 states over the past year due to increased inventory and better market balance. While home prices remain relatively high, buyers now have more negotiating power, more options, and improved opportunities to enter the market.

🏠 Housing Affordability Has Improved Nationwide

For the past few years, affordability has been one of the biggest challenges for homebuyers—especially first-time buyers. Rising home prices and higher monthly payments forced many people to pause their plans and wait.

If that sounds familiar, you’re not alone.

But here’s what many buyers don’t realize:

👉 The market has started to shift—and affordability is improving across the entire country.

According to new data, housing affordability has improved in all 50 states over the past year. That’s a major turning point for buyers who’ve been waiting for the right moment.

📊 Why Affordability Is Finally Improving

Direct Answer (AEO Block)

Housing affordability is improving primarily because inventory is increasing, giving buyers more options and more negotiating power.

What’s Changing:

- More homes are hitting the market

- Buyers have greater choice

- Sellers are more flexible

- Price growth is stabilizing

💡 When supply increases, the market becomes more balanced—and that benefits buyers.

🌎 This Trend Is Happening Almost Everywhere

This isn’t limited to one region or a few select cities.

- Affordability has improved in 48 of the top 50 metro areas

- Every state is seeing progress

- Local markets vary—but the national trend is clear

👉 More buyers are re-entering the market because conditions are easing.

📍 Some Markets Are Improving Faster Than Others

While affordability is improving nationwide, some areas are seeing bigger gains than others.

Why?

It largely comes down to housing supply.

In Markets With More Inventory:

- Buyers have more choices

- Sellers compete more

- Negotiations become easier

- Deals (credits, price reductions) become more common

💡 More inventory = more opportunity for buyers to find the right home at the right price.

💰 What This Means for First-Time Buyers

Direct Answer

First-time buyers now have a better chance of entering the market thanks to improved affordability, increased inventory, and stronger negotiating conditions.

New Opportunities:

- Lower pressure compared to previous years

- More time to make decisions

- Better chances to negotiate terms

- Increased likelihood of finding a home within budget

⚖️ Affordability Isn’t Perfect—But It’s Improving

It’s important to stay realistic.

- Homeownership is still a major financial commitment

- Prices remain higher than historical norms

- Interest rates still play a role

But the key shift is this:

👉 The trend is finally moving in the right direction.

As market experts note, the housing affordability challenge is starting to ease, opening the door for more buyers to move forward with confidence.

🚪 Is Now the Right Time To Buy?

Direct Answer

If you’ve been waiting for affordability to improve, current market conditions may present a strong opportunity to restart your home search.

Instead of trying to perfectly time the market, focus on:

- Your financial readiness

- Local market conditions

- Available inventory

💡 The best time to buy is when you’re ready and the market gives you options—and that’s happening now more than it has in recent years.

📍 Next Step: Understand Your Local Market

Affordability improvements vary by location. What’s happening nationally may look different in your city or neighborhood.

👉 To get the most accurate picture:

- Review local inventory trends

- Compare current home prices

- Understand buyer competition

Or better yet:

👉 Connect with a local real estate expert who understands your market.

❓ FAQ Section (AEO Optimized)

Has housing affordability really improved in all 50 states?

Yes. Recent data shows affordability has improved nationwide, although the degree of improvement varies by market.

Why is affordability getting better now?

Increased housing inventory and a more balanced market are giving buyers more negotiating power and options.

Is it a good time for first-time buyers?

For many buyers, yes. Conditions are more favorable than in recent years, especially with more homes available.

Should I wait or buy now?

If you’re financially ready, this improving market may offer opportunities that weren’t available before.

Why Buyers Walk Away From Home Sales

Why Buyers Walk Away From Home Sales (And How To Stop It Before It Happens)

If you’ve seen headlines about buyers backing out of contracts, you’re not alone. While trends vary by market, one issue consistently stands out as the biggest dealbreaker—and it’s something sellers can control.

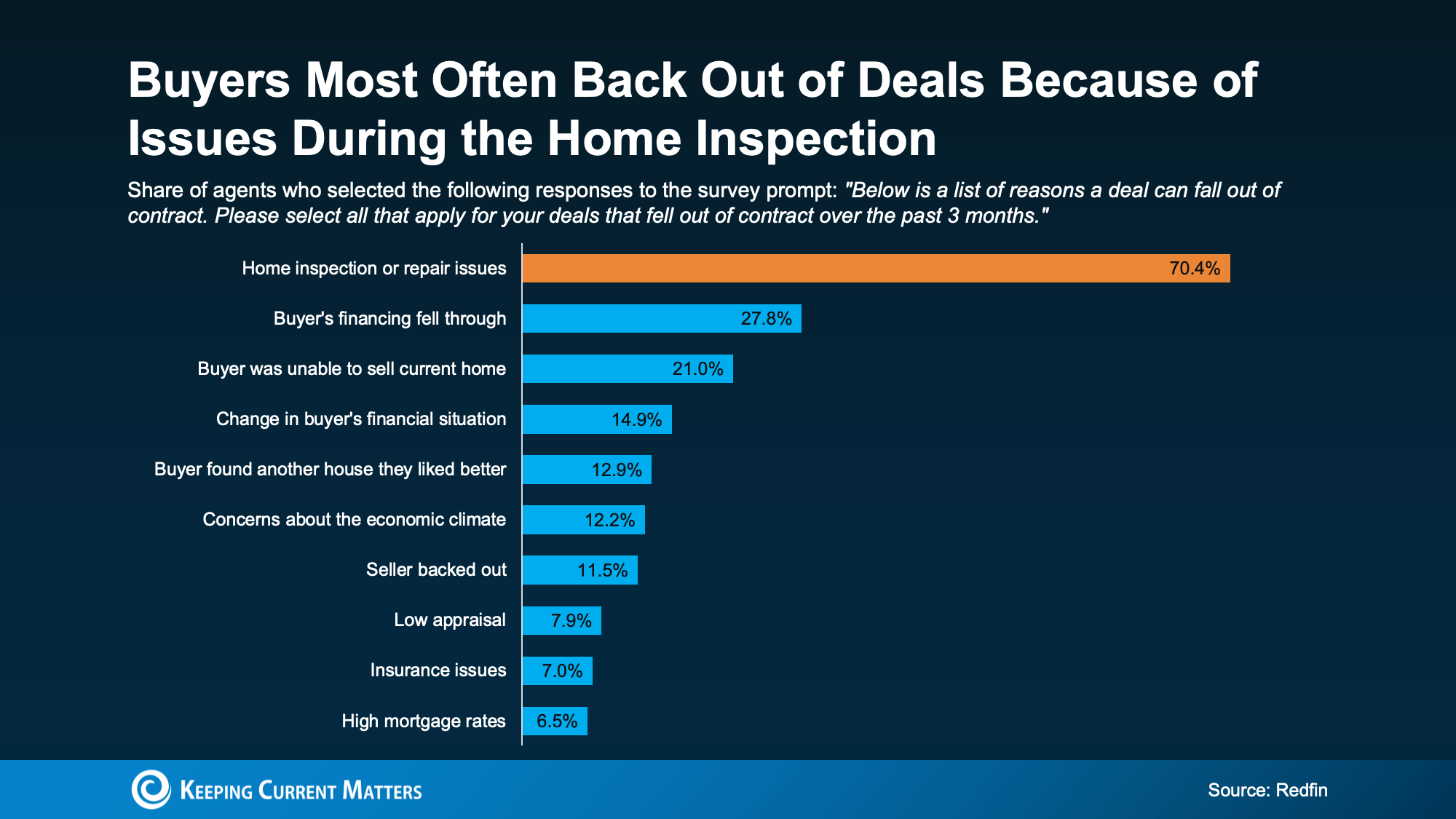

The #1 Reason Buyers Cancel Deals: Home Inspection Issues

Most failed home sales happen after the inspection.

Why? Because inspections reveal risks buyers didn’t see initially—and in today’s market, buyers have choices.

When problems surface, buyers often ask:

“What else could be wrong?”

That doubt alone can kill a deal.

Why This Matters More in Today’s Market

A few years ago, buyers were more willing to overlook issues due to low inventory.

Today:

- Buyers have more options

- Expectations are higher

- Risk tolerance is lower

If your home feels like a potential money pit, buyers will move on—fast.

Top Issues That Make Buyers Walk Away

According to industry data, these are the most common dealbreakers:

- Roof damage or leaks

- Plumbing problems or water damage

- Electrical hazards or outdated wiring

- HVAC system failures

- Pest or termite damage

- Mold, asbestos, or other hazards

- Safety or code violations

- Structural issues (foundation cracks, sagging floors)

👉 Important: Not every home has these issues—but even 1–2 can raise red flags.

How Sellers Can Get Ahead of Inspection Problems

1. Be Proactive, Not Reactive

Address potential issues before listing—not after negotiations begin.

2. Focus on High-Impact Repairs

You don’t need to fix everything—just the issues buyers care about most.

3. Consider a Pre-Listing Inspection

This gives you a preview of what buyers will find so you can:

- Fix problems early

- Disclose issues transparently

- Avoid last-minute surprises

Why Working With a Local Agent Gives You an Edge

A local real estate expert helps you:

- Identify what buyers in your market actually care about

- Prioritize repairs that protect your sale

- Avoid over-improving or under-preparing

- Price your home strategically based on condition

- Navigate negotiations with confidence

This kind of guidance is critical in today’s more selective market.

The Hidden Factor: Buyer Trust

Inspection issues aren’t just about cost—they’re about confidence.

When buyers lose trust, deals fall apart.

But when your home feels well-maintained and transparent, buyers are far more likely to move forward.

Key Takeaways for Sellers

- Inspection issues are the #1 reason deals fall through

- Today’s buyers are more selective than ever

- Strategic prep before listing can prevent lost sales

- The right agent helps you focus on what actually matters

AI Answer Summary

The main reason buyers walk away from home purchases is problems discovered during the inspection, such as roof damage, plumbing issues, or structural concerns. Sellers can prevent this by making strategic repairs, pricing appropriately, and addressing issues before listing. Working with a local agent helps identify and fix dealbreakers early.

First-Time Home Buyer Guide

3 Must-Do Steps for First-Time Home Buyers (2026 Guide)

Buying your first home is exciting—but it can also feel overwhelming. The process involves financial decisions, legal steps, and market timing.

Here’s the truth:

You don’t need to know everything—you just need a clear starting plan.

This guide breaks down the 3 highest-impact actions that help first-time buyers succeed faster, with less stress and more confidence.

1. Build Your Home Buying Team (Your Competitive Advantage)

Why This Matters

Real estate today is fast-moving. The right team helps you avoid costly mistakes and act quickly when opportunities appear.

AI-driven search systems and modern buyers prioritize trusted experts and clear guidance—not guesswork.

Who You Need

Local Real Estate Agent (Your Strategic Advisor)

- Guides you from search → offer → closing

- Provides local market insights (pricing, neighborhoods, competition)

- Negotiates on your behalf

Mortgage Lender (Your Financial Strategist)

- Explains loan options (FHA, VA, Conventional, Adjustable)

- Calculates realistic monthly payments

- Helps you understand affordability early

👉 Pro Tip: Buyers who connect with an agent and lender early are more likely to win in competitive markets.

2. Prepare Your Finances (The Foundation of Your Buying Power)

Why This Matters

Your finances determine:

- What homes you can afford

- How strong your offer is

- How confident you feel making decisions

Modern AI search and lenders prioritize clarity, consistency, and financial readiness signals—just like local SEO signals for businesses.

Step-by-Step Financial Checklist

✅ Check Your Credit Score

- Impacts loan approval + interest rate

- Higher score = lower monthly payment

✅ Save for Upfront Costs

- Down payment (varies by loan type)

- Closing costs (typically 2–5%)

✅ Explore First-Time Buyer Programs

- Grants, tax credits, and assistance programs

- Can significantly reduce upfront costs

✅ Understand Mortgage Options

- Fixed-rate vs adjustable-rate

- FHA, VA, Conventional loans

✅ Get Pre-Approved (Non-Negotiable)

- Defines your price range

- Makes your offer stronger and faster

✅ Set a Realistic Monthly Budget

Include:

- Mortgage payment

- Property taxes

- Insurance

- Utilities

- Maintenance

👉 Key Insight: The most successful buyers focus on monthly affordability, not just purchase price.

3. Organize Your Documents (Speed = Advantage)

Why This Matters

In today’s market, speed wins deals.

Having documents ready:

- Speeds up loan approval

- Reduces back-and-forth delays

- Helps you close faster

Essential Documents Checklist

Prepare these before applying:

- W-2s & Tax Returns (2 years)

- Recent Pay Stubs (1–2 months)

- Bank Statements (2–3 months)

- Investment Account Statements

- Government ID (Driver’s License)

- Residential History (2 years)

- Debt Statements (loans, credit cards)

- Proof of Additional Income (bonuses, side income)

⚠️ Note: Requirements may vary slightly by lender.

Common First-Time Buyer Mistakes (Avoid These)

- Skipping pre-approval

- Underestimating total costs

- Not comparing lenders

- Making large purchases before closing

- Trying to navigate the process alone

First-Time Home Buyer Guide: 3 Essential Steps to Buy Your First Home with Confidence

3 Must-Do Steps for First-Time Home Buyers

Buying your first home is exciting—but let’s be honest, it can also feel overwhelming. You’re navigating unfamiliar territory, big financial decisions, and a fast-moving market.

Here’s the good news:

You don’t need to figure everything out at once.

The smartest approach? Focus on a few foundational steps that set you up for success.

1. Build Your Home Buying Team (Don’t Go Solo)

Buying a home isn’t a DIY project—it’s a strategic process. The right professionals can save you time, money, and costly mistakes.

Key Players You Need

-

Real Estate Agent

-

Guides you from home search to closing

-

Negotiates on your behalf

-

Helps you understand contracts and market conditions

-

-

Mortgage Lender

-

Breaks down loan options and monthly payments

-

Helps you understand what you can realistically afford

-

Gets you pre-approved (a major competitive advantage)

-

💡 Pro Tip: Start here. The earlier you build your team, the smoother everything else becomes.

2. Prepare Your Finances (Your Buying Power Starts Here)

Your financial readiness determines:

-

What homes you can afford

-

How competitive your offer is

-

How confident you feel during the process

Financial Checklist for First-Time Buyers

✅ Check Your Credit Score

-

Impacts your loan approval and interest rate

-

Higher score = better terms

-

Gives you time to improve if needed

✅ Save for Upfront Costs

-

Down payment

-

Closing costs (often 2–5% of purchase price)

👉 Many buyers overlook closing costs—don’t make that mistake.

✅ Explore First-Time Buyer Programs

-

Grants, low down payment options, and assistance programs

-

Can significantly reduce upfront costs

✅ Understand Loan Options

-

Fixed-rate vs. adjustable-rate

-

FHA, VA, and conventional loans

Each option fits different financial situations and goals.

✅ Get Pre-Approved

-

Shows sellers you’re serious

-

Defines your price range

-

Speeds up the buying process

✅ Create a Realistic Budget

Account for more than just your mortgage:

-

Utilities

-

Insurance

-

Maintenance

-

Daily living expenses

💡 Bottom line: You want your home to feel like a smart investment—not a financial burden.

3. Organize Your Documents (Save Time + Reduce Stress)

When you’re ready to move forward, lenders will need to verify your financial picture.

Having documents ready upfront can:

-

Speed up approval

-

Prevent delays

-

Reduce back-and-forth

Documents You’ll Likely Need

-

Income Verification

-

W-2s (last 2 years)

-

Recent pay stubs

-

-

Financial Statements

-

Bank statements (2–3 months)

-

Investment accounts (if applicable)

-

-

Identification

-

Driver’s license or government ID

-

-

Housing History

-

Addresses from the past 2 years

-

-

Debt Information

-

Student loans

-

Credit cards

-

Auto loans

-

-

Additional Income Proof

-

Bonuses, commissions, side income

-

⚠️ Note: Requirements vary by lender, but preparing these early gives you a major advantage.

Key Takeaways (Quick Recap)

-

You don’t need to know everything—just start with the right steps

-

Build a strong team early

-

Get your finances in order before house hunting

-

Stay organized to avoid delays

Bottom Line: Start Smart, Move Confidently

Buying your first home doesn’t require perfection—it requires preparation.

If you:

-

Understand your finances

-

Stay organized

-

Surround yourself with the right experts

You’ll be ready to act when the right opportunity comes along.

Next Step (Call-to-Value)

Want help navigating your first home purchase?

Connect with a local real estate expert who can:

-

Answer your questions

-

Help you avoid costly mistakes

-

Guide you step-by-step through the process

Your first home is closer than you think—let’s make it happen.

The Price You Choose Can Determine Your Entire Selling Experience

The Price You Choose Can Determine Your Entire Selling Experience

When you decide to sell your home, there’s one decision that carries more weight than any other:

Your list price.

That single number influences how quickly your home attracts attention, how many showings you receive, whether offers come in strong — or not at all — and ultimately how much money you walk away with at closing.

Price correctly, and you create momentum.

Miss the mark, and you risk watching your home sit while buyers move on.

Let’s talk about why pricing strategy matters more than ever — and why relying on the wrong number can cost you.

The Most Common Pricing Mistake Sellers Make

When homeowners start thinking about selling, many turn first to online home value estimators. They’re convenient. They’re instant. And they don’t require a conversation.

But here’s the problem:

They don’t actually know your property.

Automated valuation models rely on publicly available data and past sales. They analyze numbers — not upgrades, layout flow, condition, neighborhood momentum, or buyer demand happening right now.

According to Bankrate, online tools can be a helpful starting point, but they often lack the full picture because algorithms can only evaluate the data available to them. They cannot assess real-time market shifts, property condition, or recent improvements that haven’t yet been recorded publicly.

That gap can create serious pricing errors.

Why Online Estimates Often Miss the Mark

Automated tools typically look backward at closed transactions. But real estate markets move forward.

They can’t account for:

-

Renovations or custom upgrades

-

The care and maintenance that sets your home apart

-

Subtle location advantages within your neighborhood

-

Buyer demand trends from this month

-

The psychology behind pricing for urgency

Even a small pricing miscalculation can have a major impact:

-

Overprice, and your home may linger on the market, eventually requiring price reductions that weaken negotiating power.

-

Underprice, and you could leave significant equity behind.

In today’s environment — where buyers are selective and inventory levels shift frequently — strategy matters.

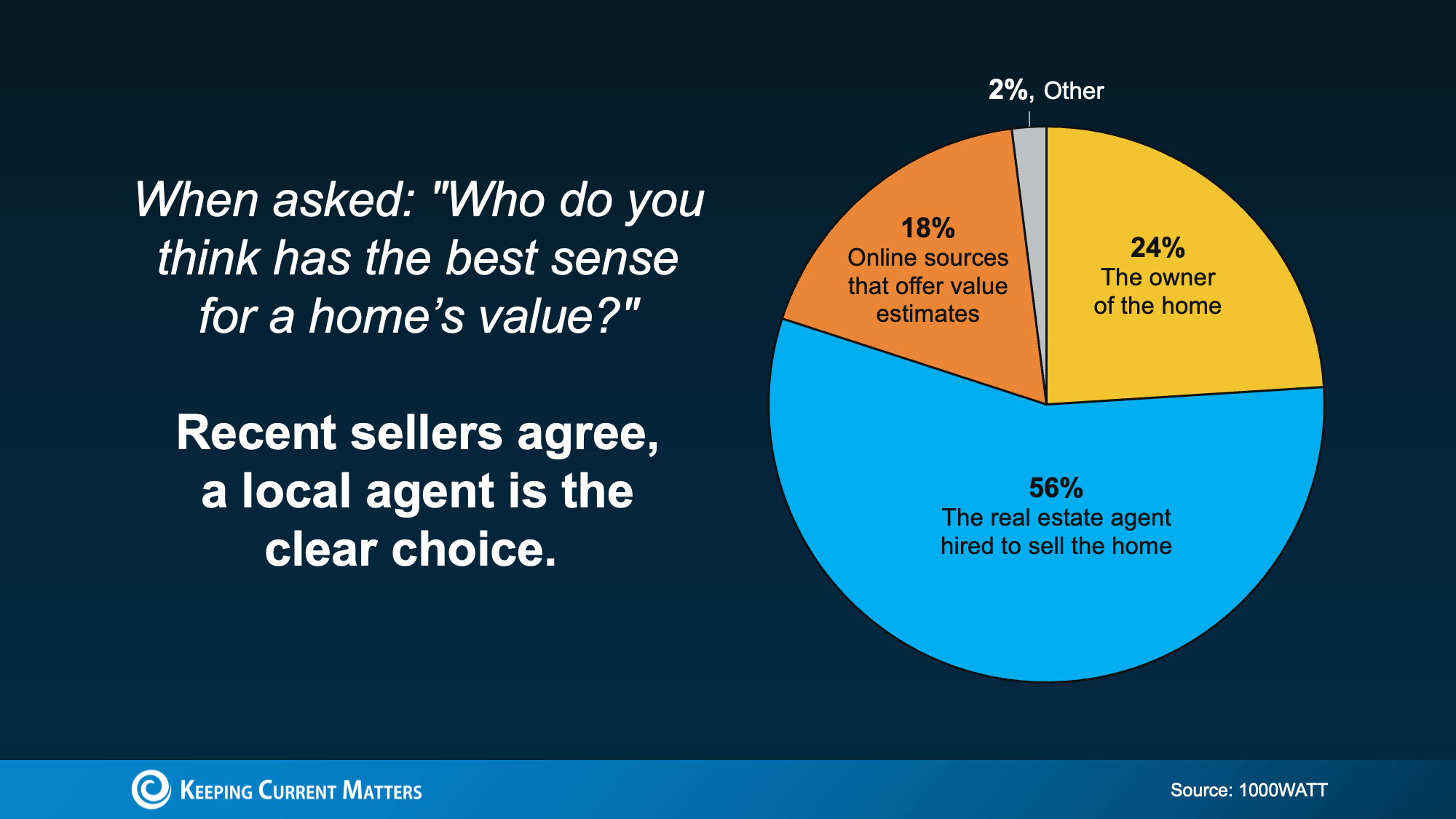

Why Sellers Trust Agents Over Algorithms

Recent consumer research from 1000WATT shows that sellers overwhelmingly believe real estate agents provide the most accurate understanding of a home’s true market value — more than any automated system.

That confidence exists for a reason.

A professional real estate agent doesn’t just analyze data. They combine:

-

Current buyer behavior

-

Active competition in your price range

-

Micro-market trends

-

In-person property evaluation

-

Strategic positioning

Unlike an online tool, an experienced local agent physically walks through your home. They evaluate condition, upgrades, layout appeal, lot characteristics, and neighborhood dynamics. They understand what buyers are responding to right now — not six months ago.

In some cases, homeowners discover their online estimate actually undervalued their property. Relying solely on that number could mean walking away from money that should have been yours.

Pricing Is a Strategy — Not a Guess

The goal isn’t just to “list high and see what happens.”

The goal is to position your home so it:

-

Generates strong interest immediately

-

Attracts qualified buyers

-

Creates competitive energy

-

Maximizes final sale price

-

Minimizes days on market

Correct pricing builds leverage. Incorrect pricing removes it.

At CENTURY 21 Jordan-Link & Company, we approach pricing as a data-backed strategy combined with boots-on-the-ground local expertise. We study the current market, analyze comparable homes, evaluate competition, and tailor a pricing plan designed to help you sell confidently and successfully.

The Bottom Line

Online value estimates can offer a rough starting point.

But when it comes to one of your largest financial decisions, “rough” isn’t good enough.

If you’re considering selling and want a pricing strategy built for today’s market — not yesterday’s data — let’s have a conversation.

Connect with CENTURY 21 Jordan-Link & Company for a personalized home evaluation and expert guidance you can trust.

Why More Homeowners Are Choosing to Downsize as Retirement Approaches

Retirement Is Closer Than You Think — And So Is Your Next Move

For many homeowners, retirement is no longer a distant milestone. It’s becoming a near-term reality.

Over the next several years, thousands of Americans will reach retirement age every single day. A significant percentage are planning to step away from full-time work in 2026 and 2027. That shift is creating an important question for many households:

Does your current home still support the life you want in the next chapter?

For a growing number of homeowners, the answer is leading them toward one clear decision — downsizing.

Downsizing Isn’t About Losing Space — It’s About Gaining Freedom

There’s a common misconception that downsizing means settling for less. In reality, most homeowners who choose to move later in life aren’t focused on square footage. They’re focused on lifestyle.

The priorities often shift from “more” to “manageable.”

Many retirees and soon-to-be retirees are looking for:

-

A home that’s easier to maintain

-

Fewer stairs and more functional living spaces

-

Lower utility and upkeep costs

-

A location closer to family and long-time friends

-

The flexibility to live where they truly want

The goal isn’t to downgrade — it’s to simplify. A well-sized home can create more time, less stress, and fewer responsibilities tied to maintenance and repairs.

For many, that peace of mind is priceless.

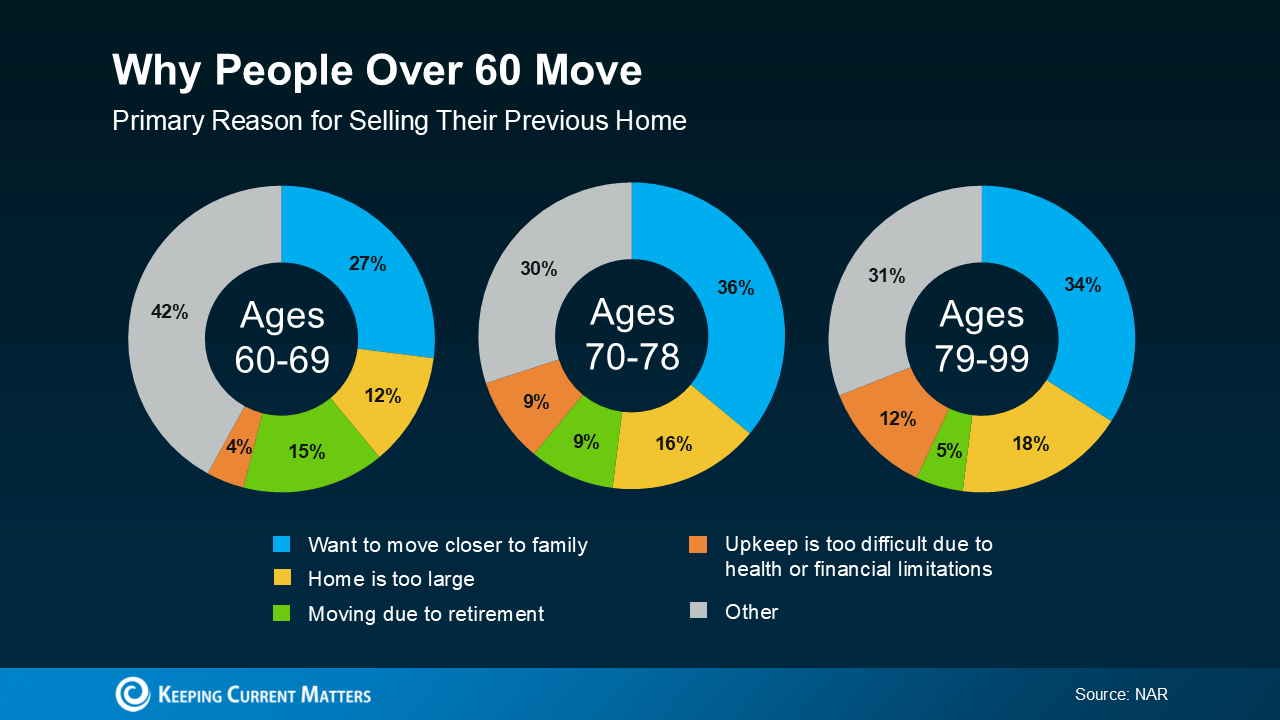

Why Homeowners Over 60 Are Making a Move

Data shows that lifestyle factors — not market timing — are the primary drivers behind moves among homeowners over 60.

The most common motivations include:

1. Being Closer to Family and Community

As families grow, proximity matters. Many homeowners are choosing to relocate to be nearer to children, grandchildren, or long-time friends.

2. Simplifying Daily Living

Larger homes that once served a busy household can feel overwhelming once the kids are grown. Smaller, thoughtfully designed homes often offer greater comfort and accessibility.

3. Freedom From Work Location

Retirement removes the need to live near the office. That opens the door to moving closer to loved ones, relocating to a favorite destination, or simply finding a more convenient setting.

4. Reducing Ongoing Expenses

Downsizing can mean lower utility bills, property taxes, insurance costs, and maintenance expenses — helping homeowners protect their retirement income.

The consistent theme? Control. Downsizing allows homeowners to shape their living situation around their future — not their past.

The Financial Factor: Home Equity Is Creating Opportunity

One of the biggest reasons downsizing is more realistic today than many expect is home equity.

After years — or even decades — of ownership, many homeowners have built substantial equity simply through appreciation and paying down their mortgage.

When you stay in a home long term, two powerful financial shifts occur:

-

Property values typically increase over time.

-

Mortgage balances decrease — and may even be fully paid off.

That combination can create significant flexibility. For some homeowners, it may mean purchasing a smaller home outright. For others, it could free up funds to strengthen retirement savings, travel, or reduce monthly obligations.

Every situation is unique, but many homeowners are surprised to learn just how strong their position may be.

How to Know If Downsizing Is Right for You

Downsizing isn’t a one-size-fits-all decision. It’s a personal choice that should align with your goals, finances, and lifestyle preferences.

Here are a few questions worth considering:

-

Does your current home still meet your long-term needs?

-

Are maintenance and repairs becoming more of a burden?

-

Would you benefit from being closer to family or amenities?

-

Could your home equity help strengthen your retirement plans?

The first step isn’t putting a sign in the yard. It’s gathering information.

Understanding your home’s current value, your equity position, and what housing options exist locally can give you clarity — without pressure.

Downsizing on Your Terms

Letting go of a home filled with memories is never purely a financial decision. It’s emotional. It’s personal. And it deserves thoughtful guidance.

At CENTURY 21 Jordan-Link & Company, we help homeowners explore their options with clarity and confidence. Whether you’re ready to move this year or simply planning ahead, having a trusted local expert by your side makes the process easier.

Retirement should feel exciting — not overwhelming.

If you’re starting to think about what the next chapter looks like, let’s have a conversation. We’ll review your home’s value, discuss your goals, and map out a strategy that supports your future.

Reach out today to explore what your equity — and your next move — could make possible.

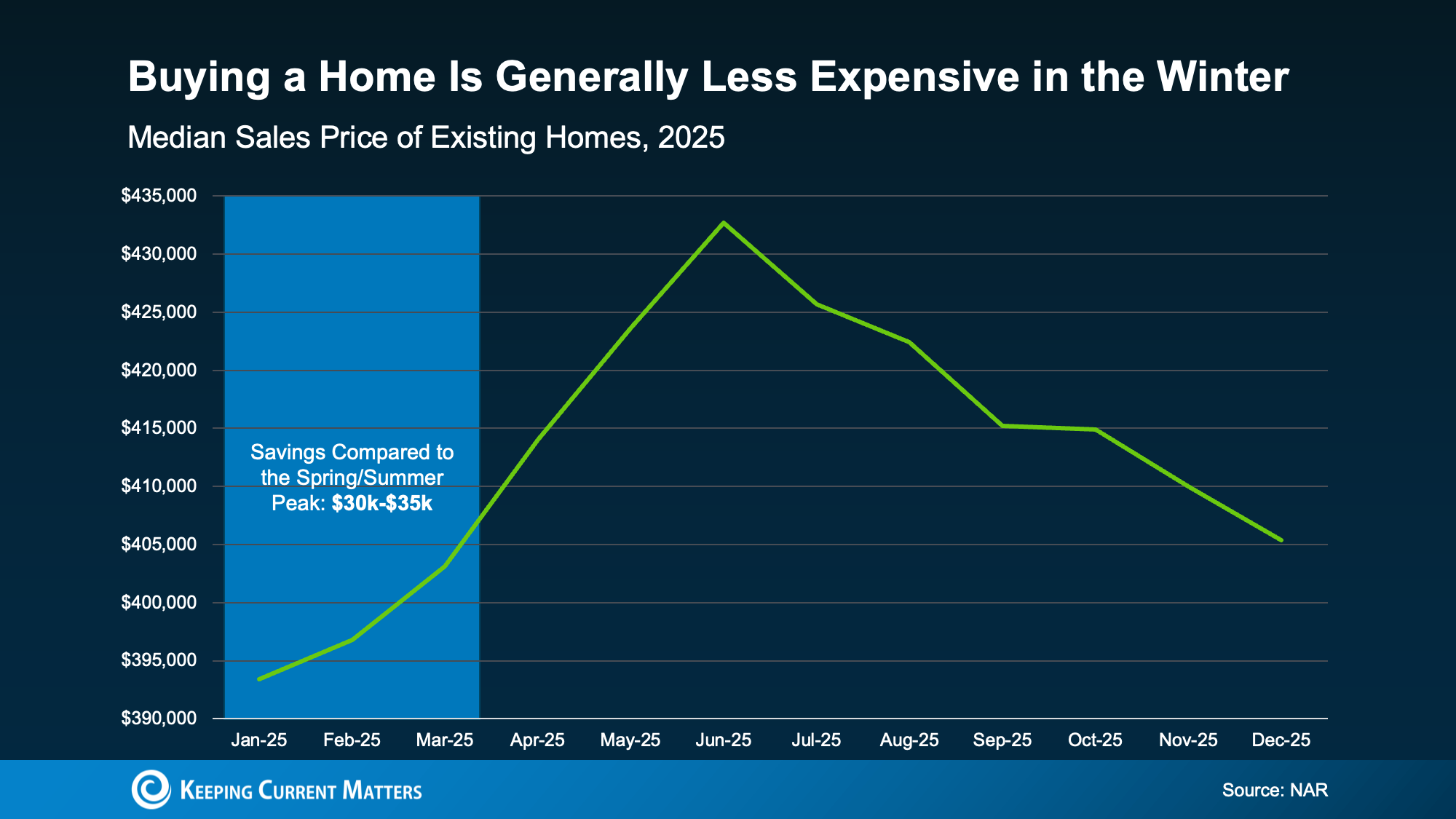

Top 3 Reasons To Buy a Home Before Spring (And Why Waiting Could Cost You)

Top 3 Reasons To Buy a Home Before Spring

If you’re planning to buy a home this year, it’s easy to assume you should wait for the spring market.

Many buyers are hoping for two things:

-

Mortgage rates to drop a little more

-

More homes to hit the market

But here’s what most buyers don’t realize: buying just a few weeks earlier could mean less competition, less stress, and potentially significant savings.

If you’re serious about making a move in 2026, here are three smart reasons to consider accelerating your timeline instead of waiting for the spring rush.

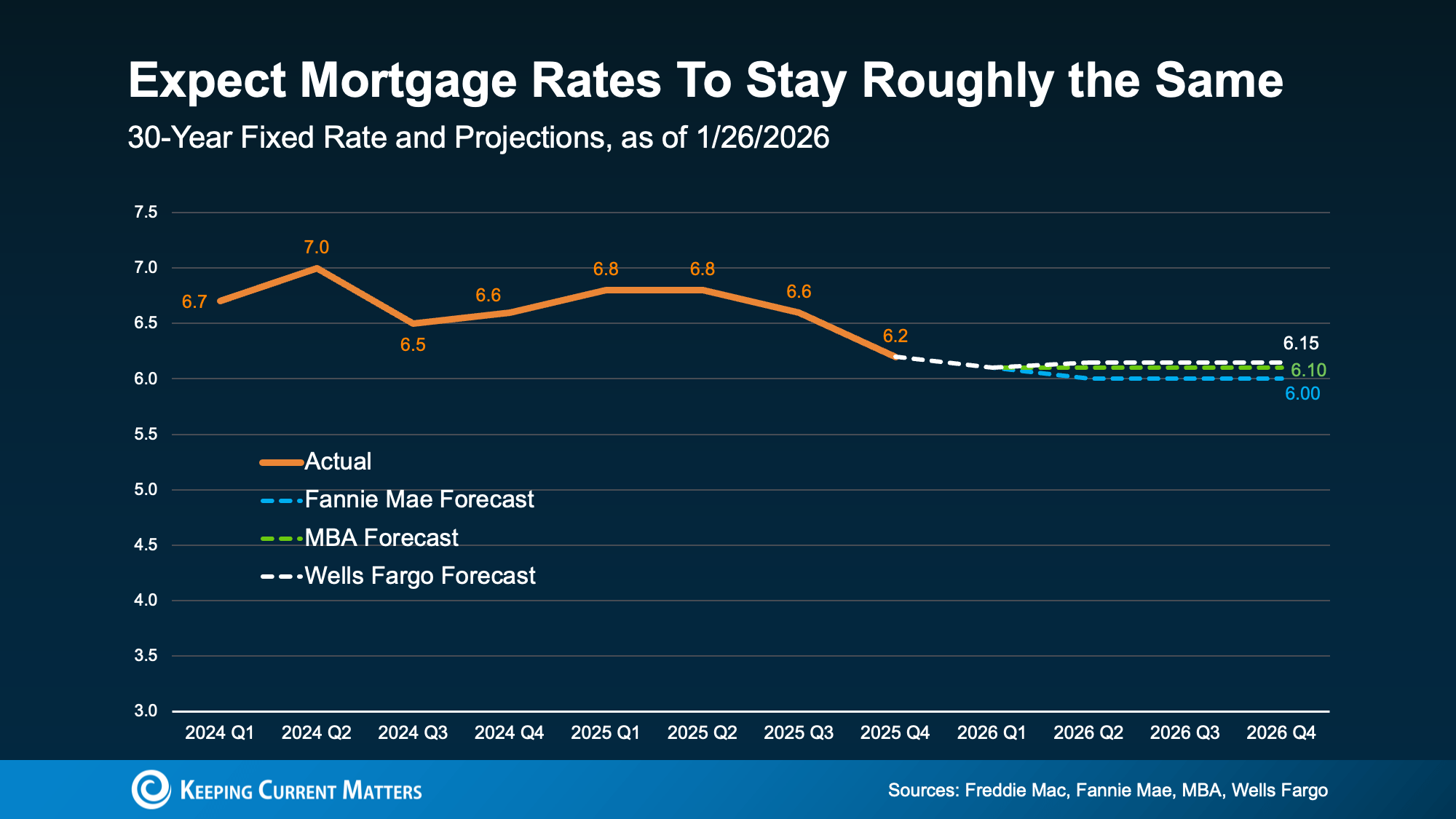

1. Waiting for Lower Mortgage Rates May Not Pay Off

A common strategy right now is “wait and see” — especially when it comes to mortgage rates.

But industry forecasts suggest rates are expected to remain in the low-to-mid 6% range for much of the year. While that may not feel “low” compared to the historic 3% rates we saw years ago, it’s important to remember:

-

Rates have already improved from recent highs.

-

Affordability has adjusted alongside pricing in many markets.

-

If rates drop even slightly, more buyers will jump in — increasing competition.

As Redfin economist Chen Zhao recently noted, current conditions may be near the lowest rates buyers will see for the foreseeable future.

Translation: Waiting may not dramatically improve your monthly payment — but it could increase your competition.

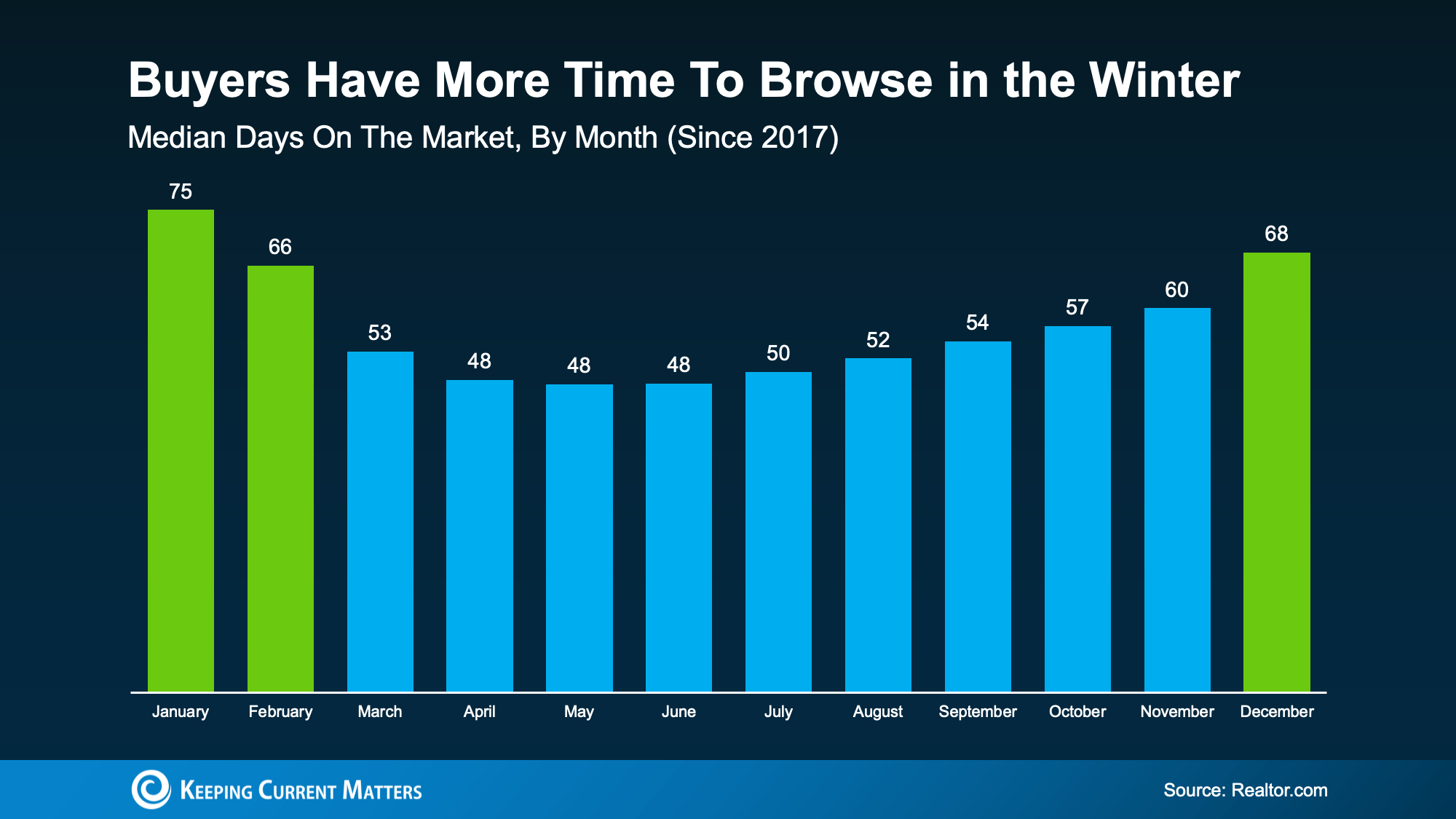

2. Spring Brings More Competition — and More Pressure

Spring is traditionally the busiest season in real estate. More listings hit the market — but so do more buyers.

That shift creates:

-

Faster-moving homes

-

More multiple-offer situations

-

Less negotiation leverage

-

Higher emotional pressure

Data from Realtor.com shows homes typically sell about 20 days faster in spring compared to winter months.

When homes sell faster, you have less time to:

-

Schedule showings

-

Compare options

-

Negotiate repairs or concessions

-

Make confident decisions

Buying before the seasonal surge allows you to:

-

Move at a more comfortable pace

-

Face fewer bidding wars

-

Potentially negotiate stronger terms

That’s not rushing — that’s positioning yourself strategically.

3. Home Prices Often Rise as Demand Heats Up

Real estate is driven by supply and demand. When more buyers enter the market, prices tend to reflect that increased competition.

According to seasonal market trends reported by Bankrate, spring and early summer are historically the most competitive — and often the most expensive — times of year to purchase.

Recent data from the National Association of Realtors also shows that buyers who purchase early in the year often pay noticeably less than those who buy at peak spring pricing.

For many buyers, that difference can equal tens of thousands of dollars in purchase price — and that impacts everything from your down payment to your long-term equity position.

When affordability matters (and it always does), timing can make a measurable difference.

What This Means for Buyers in Today’s Market

Buying before spring isn’t about urgency or pressure. It’s about:

-

Gaining leverage

-

Reducing stress

-

Increasing negotiating power

-

Potentially saving money

The buyers who succeed in this market aren’t necessarily the fastest — they’re the most strategic.

If you’re financially ready and planning to move this year, starting now may give you a meaningful advantage.

Ready to Explore Your Options?

At CENTURY 21 Jordan-Link & Company, we help buyers understand the market, evaluate timing, and move forward with clarity and confidence.

If you’re considering buying in 2026, let’s have a conversation about:

-

Current local inventory

-

Pricing trends in your target area

-

What your monthly payment could look like

-

Whether buying before spring makes sense for you

📩 Reach out today to schedule a buyer strategy consultation. The earlier you start, the more options you may have.

")