Getting a mortgage can be a bit like running a marathon. It’s a long process, and there are many steps to take. Two of the most misunderstood stages are pre-qualification and pre-approval. Both are critical, but they serve different purposes. Pre-qualification is like a warm-up; it gives you an idea of how much you may be able to borrow based on your self-reported financial data. Pre-approval, on the other hand, is like the starting gun. It involves a more in-depth look at your finances, including a credit check, and results in a conditional commitment from the lender for a particular loan amount. So, lace up your shoes, and let’s break down these two mortgage categories.

Exploring Mortgage Prequalification

In the pursuit of homeownership, one encounters the terms ‘pre-qualification’ and ‘pre-approval,’ both pivotal steps in the mortgage process. Diving into the concept of pre-qualification, you share your financial information, such as income, assets, and debts. This process, which usually doesn’t entail a credit check, can be wrapped up within a few days. The prequalification stage is particularly insightful as it gives you a rough idea of the potential loan amount you might qualify for. You can kickstart the process by discussing your financial goals and mortgage options with the lender. Once done, you’ll receive a prequalification letter, outlining an estimate of your possible borrowings.

How to Get Prequalified for a Mortgage

Securing mortgage pre-qualification requires a few easy steps. To get the ball rolling, you need to provide the lender with basic financial details. This could be done online or over a friendly phone call. This conversation is a golden opportunity to hash out your financial goals and discuss the mortgage options at your disposal. After this, you will receive a pre-qualification letter. This document is like your personal financial compass, pointing you in the direction of your potential borrowing capacity. It’s a snapshot of your financial standing, and it can help you set realistic expectations for your home buying budget.

Diving into Mortgage Preapproval

Moving further into the home buying process, it’s time to discuss mortgage preapproval. More intensive than pre-qualification, pre-approval necessitates a detailed financial examination. This includes a credit check and gathering of financial documents such as W-2s, tax returns, and bank statements. The outcome of this analysis? A conditional commitment from the lender for a precise loan amount.

The steps to secure a mortgage pre-approval are slightly more demanding. It commences with a formal mortgage application. You’ll then provide the necessary financial documentation for the lender to verify. A credit check follows, conducted by the lending institution. The final product is a pre-approval letter, specifying the loan amount and conditions for a set period.

Here’s a friendly tip: don’t confuse pre-approval with a final loan commitment. It’s a step closer, though!

Steps to Securing a Mortgage Preapproval

Following the path to mortgage pre-approval entails a series of steps. Kick things off by completing a formal mortgage application, which is a detailed questionnaire about your financial situation. Then, gather all necessary financial documents such as pay stubs, tax returns, and bank statements for verification by the lender.

Next, the lender conducts a credit check to assess your creditworthiness. Remember, this is a hard inquiry which may impact your credit score slightly.

Once the lender verifies your information and assesses your credit, you’ll receive a pre-approval letter. This letter indicates the loan amount you’re approved for and its conditions, and it’s typically valid for 60-90 days.

Keep in mind that preapproval is not a loan guarantee, but it does put you a step closer to securing a home loan.

Pre-qualification vs Pre-approval: The Core Differences

Distinguishing between pre-approval and pre-qualification in the mortgage process can be a bit puzzling. In the simplest terms, pre-qualification is an initial evaluation of your financial status, offering an estimated loan amount based on the information you provide. It’s a quick process and can often be done without a credit check. Pre-approval, on the other hand, is a more thorough validation of your financial situation. It involves a hard credit check and documentation verification, resulting in a conditional commitment from the lender for a precise loan amount. In essence, pre-approval is a more accurate, albeit time-consuming, assessment of your borrowing capacity compared to pre-qualification.

Impact of Prequalification and Preapproval on Credit Scores

When it comes to your credit score, both pre-qualification and pre-approval can leave distinct marks. The process of pre-qualification often only requires a soft inquiry, which doesn’t typically impact your credit score. This soft pull allows lenders to provide an estimated loan amount based on basic financial information you’ve divulged.

On the flip side, pre-approval usually necessitates a hard credit inquiry. This rigorous credit check can temporarily lower your credit score by a few points. But don’t fret. This minor dip is often quickly recovered, and the process offers a more precise gauge of your borrowing ability. It’s a small price to pay for the added certainty in your home buying process.

In the pre approval vs pre qualification debate, it’s clear each has its own impact on your credit score, with varying levels of severity and benefits.

7 Things Mortgage Lenders Consider for Preapproval

Getting a green light on your mortgage pre-approval revolves around several factors. So, let’s look at the seven criteria that lenders evaluate during this phase.

Credit score and history: Your credit score serves as a reflection of your financial responsibility. Lenders review this alongside your credit history to assess your reliability as a borrower.

Income and employment stability: Regular income and a stable job reassure lenders that you can meet monthly repayments.

Debt-to-income ratio: This measures your total monthly debts against your gross monthly income. A lower ratio suggests better financial health.

Assets and savings: Lenders may consider your assets and savings as a safety net in case you default on the loan.

Down payment amount: A larger down payment often results in better loan terms as it reduces the lender’s risk.

Previous bankruptcies or foreclosures: Any history of bankruptcy or foreclosure could affect your preapproval, depending on how recent they were.

Property details and appraisal: The value and condition of the property you’re buying can impact the loan amount. The lender may request an appraisal to verify the property’s worth.

Remember, getting pre-approved is a conditional commitment from the lender. It typically involves a more rigorous process compared to pre-qualification. In the end, it’s your financial responsibility and preparation that’ll make the difference.

Do You Need to Spend the Entire Preapproved Amount?

Is it necessary to utilize the full amount that has been pre-approved for your mortgage? The simple answer is no. The amount you’ve been preapproved for by your mortgage lender sets the upper limit, but you’re not required to go to that extreme.

In fact, it’s often a good idea to borrow less than your maximum pre-approval amount. Keep in mind other financial obligations or future plans that may impact your budget. Rather than stretching your finances thin, aim for a mortgage that comfortably fits within your financial capacity. This approach can help avoid potential financial stress and keep you on track to achieve your long-term financial goals. Remember, a preapproval simply provides a ceiling, it’s up to you to decide the final home loan sum.

Choosing the Right Path: Prequalification or Preapproval

Deciding between pre-qualification or pre-approval is pivotal in the home buying process. A pre-qualification gives you a ballpark figure of how much you might borrow based on your self-reported financial information. It’s a great starting point, particularly for those stepping into the housing market for the very time.

On the flip side, a mortgage pre-approval is a more concrete step. It involves a thorough review of your financial situation, including a credit check and documentation submission. This results in a conditional loan commitment from the lender, signaling to sellers that you’re serious and financially prepared to buy.

The path you choose depends largely on your situation. Are you still browsing or ready to make an offer? Pre-qualification is a quick, preliminary step, but preapproval gives you more weight in competitive markets. So, make the choice that suits your home buying stage.

Common Misconceptions About Prequalification and Preapproval

There’s some confusion surrounding pre approval vs pre qualification that need to be clarified. One common belief is that pre-qualification guarantees loan approval. In reality, it’s only an initial assessment based on self-reported financial information, not a loan promise. Another misconception is that pre-approval equals a final loan commitment. Actually, it’s an in-depth financial review leading to a conditional loan agreement, not an outright guarantee. Differentiating between these two steps is paramount as they serve distinct purposes in the home buying process. Understand their respective roles to navigate your home buying process effectively. Remember, both steps hold value at different stages of your house-hunting adventure.

Commercial Real Estate: Navigating the New Landscape

The commercial real estate (CRE) market is currently experiencing a profound metamorphosis, driven by an amalgamation of factors such as technological breakthroughs, evolving consumer habits, and economic ambiguities. While these shifts present obstacles, they also unveil unparalleled prospects for astute investors and developers.

The Evolving Workplace

Arguably, the most pivotal change within commercial real estate (CRE) is the transformation of the workplace. The pandemic expedited the adoption of remote and hybrid work models, compelling enterprises to reassess their office space requirements. Consequently, there has been a surge in demand for flexible office spaces, co-working facilities, and suburban office locations.

Opportunities:

Adaptive Reuse: Transforming antiquated office buildings into mixed-use developments encompassing residential, retail, and office components can be exceedingly lucrative.

Suburban Office Boom: Investing in suburban office parks with amenities such as retail outlets, dining establishments, and fitness centers can leverage the burgeoning demand for decentralized work environments.

Flexible Workspace: Creating adaptable office spaces catering to the needs of small businesses and startups can provide a consistent income stream.

The Rise of E-commerce and Retail Reinvention

The e-commerce surge has reshaped the retail landscape, compelling traditional brick-and-mortar stores to either adapt or shutter. However, the demise of physical retail has been greatly exaggerated. Experiential retail, which merges shopping with entertainment and dining, is gaining momentum.

Opportunities:

E-commerce Fulfillment Centers: Investing in strategically situated warehouse and distribution centers to support the burgeoning e-commerce sector can yield substantial returns.

Experiential Retail: Developing mixed-use projects that integrate retail, dining, and entertainment can attract patrons seeking unique experiences.

Last-Mile Delivery: Investing in properties suited for last-mile delivery services, such as urban warehouses or retail spaces, can capitalize on the escalating demand for swift and convenient delivery.

Industrial Real Estate: A Strong Performer

The industrial real estate sector has exhibited remarkable resilience, propelled by robust e-commerce growth and supply chain optimization endeavors. The demand for warehouse, distribution, and logistics facilities continues to surpass supply in numerous markets.

Opportunities:

Cold Storage: Investing in cold storage facilities can benefit from the increasing demand for perishable goods and the heightened focus on food supply chain resilience.

Logistics Parks: Developing large-scale logistics parks with advanced infrastructure can attract major distribution companies and generate sustained rental income.

Data Centers: As data consumption proliferates exponentially, investing in data center properties can provide stable and high-yielding returns.

Sustainability and ESG

Environmental, social, and governance (ESG) factors are becoming increasingly paramount to investors and tenants. Sustainable buildings and developments are in high demand, offering both financial and reputational advantages.

Opportunities:

Green Building Development: Constructing or retrofitting buildings to meet green building standards can attract environmentally conscious tenants and qualify for tax incentives.

Renewable Energy Investments: Investing in renewable energy projects, such as solar panels or wind turbines, can generate additional income and enhance property value.

Conclusion

The commercial real estate landscape is both dynamic and intricate, yet it offers exhilarating opportunities for those who can discern and capitalize on emerging trends. By understanding the evolving needs of businesses and consumers, and by embracing innovation and sustainability, investors and developers can position themselves for enduring success.

Ventura City Councilwoman Liz Campos: From Eviction to Advocacy for the Homeless June 4, 2024 | Photo by Julie Leopo-Bermudez for CalMatters

Summary

Before her election to the Ventura City Council, Liz Campos was on the brink of homelessness. Today, she lives in a van and continues her fight to support others facing similar challenges.

California, home to over 172,000 homeless individuals, leads the nation in homelessness. Contrary to popular belief, many homeless people are employed. A 2017 San Francisco survey revealed that 13% of the homeless population held part-time or full-time jobs. The crisis is underscored by reports of homeless doctors in San Diego.

Liz Campos, who was elected to the Ventura City Council in late 2022, experienced homelessness shortly before taking office. A former middle school teacher, Campos has called Ventura home for over 22 years.

In the following interview, Campos shares insights into how her personal experience with homelessness shapes her views and policies as a city council member. The responses have been edited for clarity and brevity.

Q&A with Liz Campos

How has your experience with homelessness shaped your approach as a city council member?

I’ve been advocating for the homeless since my college days, where I interned at a homeless assistance program. My stance hasn’t changed since being elected. Unfortunately, I became homeless when my landlord, disagreeing with my political views, evicted me and sold the property. This personal experience has only strengthened my commitment to enforceable tenant protections in Ventura.

What policies do you propose to address homelessness in Ventura and statewide?

I believe strong tenant protections are key to preventing homelessness. Beyond that, we need basic services for the homeless like showers, laundry facilities, clothing exchanges, and “listening posts” that connect people to housing resources.

Additionally, we need to rethink the narrative around solving homelessness. Building expensive housing doesn’t help those most in need. In fact, luxury condos drive up rental prices for lower-income residents.

Regulating short-term vacation rentals is also essential. These rentals reduce available housing stock, pushing more people into homelessness. Ventura has homeless schoolchildren, which should be a top priority. Homeless children are not vagrants or criminals—they need urgent support.

What are the challenges of serving as a city council member while homeless, and how do you manage them?

While my situation is better than many—I live in a van on private property and have a permanent address—life is still difficult. I rely on a wheelchair and lack basic facilities like a kitchen and shower. The hardest part is dealing with the negative stereotypes and rhetoric about homelessness.

Despite these challenges, I remain focused on helping those who are even less fortunate than me.

What would you like people to know about those experiencing homelessness?

First and foremost, they are human beings. Not all homeless people are drug users or criminals. Take a moment to greet them, and you may be surprised by the conversation.

What can the city and state do to prevent homelessness?

The government needs to regulate vacant housing and ensure that at least 50% of new housing developments are dedicated to low-income individuals. We also need to redefine what “affordable housing” truly means and ensure that inclusionary housing policies actually benefit the lowest-income residents.

Conclusion

Liz Campos’ story highlights the urgent need for stronger tenant protections and affordable housing initiatives in California. Her advocacy for the homeless—rooted in personal experience—offers a unique perspective in addressing the homelessness crisis in Ventura and beyond.

The 2024 Presidential election is just months away. As someone considering buying or selling a home, you may wonder how elections affect the housing market.

Historically, Presidential elections have only a small, temporary impact on the housing market. Here’s what’s happened to home sales, prices, and mortgage rates during those periods.

Home Sales

During November in Presidential election years, home sales typically slow down slightly. Ali Wolf, Chief Economist at Zonda, explains:

“Usually, home sales are unchanged compared to a non-election year with the exception being November. In an election year, November is slower than normal.”

This is mainly because people feel uncertain about making big decisions during such a pivotal time. However, this slowdown is temporary. Historically, home sales bounce back in December and continue to rise the following year.

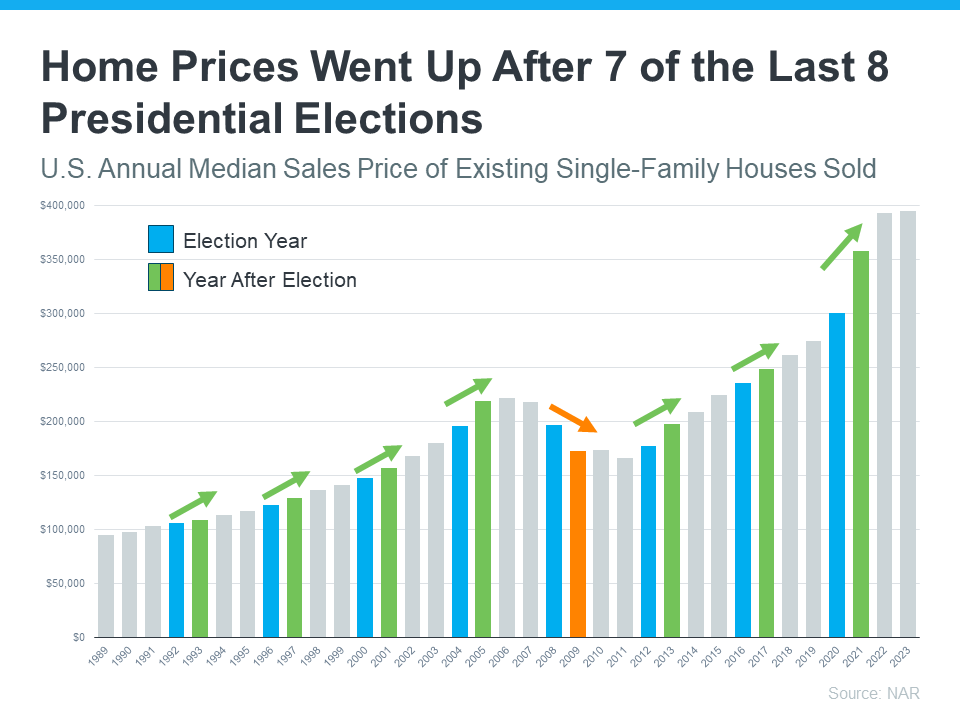

Data from the Department of Housing and Urban Development (HUD) and the National Association of Realtors (NAR) shows that after nine of the last 11 Presidential elections, home sales increased the next year.

Home Prices

Do home prices drop during election years? Not typically. Residential appraiser and housing analyst Ryan Lundquist states:

“An election year doesn’t alter the price trend that is already happening in the market.”

Home prices are resilient, generally rising year-over-year, regardless of elections. Data from NAR shows that after seven of the last eight Presidential elections, home prices increased the following year.

The only year when prices declined after an election was during the housing market crash, which was far from typical. Today’s market is different.

Mortgage Rates

Mortgage rates, which affect your monthly payment when buying a home, tend to decrease from July to November in most election years. Data from Freddie Mac shows this trend in eight of the last 11 Presidential election years.

Most forecasts expect mortgage rates to ease slightly throughout the rest of the year. This trend could benefit those looking to buy a home, as lower rates mean lower monthly payments.

What This Means for You

While Presidential elections do have some impact on the housing market, the effects are usually small and temporary. Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Historically, the housing market doesn’t tend to look very different in presidential election years compared to other years.”

For most buyers and sellers, elections don’t significantly impact their plans.

Bottom Line

While it’s natural to feel uncertain during an election year, history shows the housing market remains strong and resilient. If you have questions, reach out to a local real estate agent. They’re here to help you navigate the market, election year or not.

In the world of real estate, the ability to efficiently navigate the myriad of paperwork and deadlines is crucial. The journey of buying or selling property involves numerous steps, each with its own set of documents and timeframes. Mastering these elements not only ensures a smooth transaction but also enhances your overall experience. Today, Century 21 Jordan-Link & Company will explore several key strategies that can help transform the often-overwhelming process of real estate transactions into a manageable and streamlined experience.

Documenting the Timeline

Creating a detailed timeline is a fundamental step in managing the complex schedule of a real estate transaction. By outlining every crucial milestone and deadline, you establish a clear path forward. This not only serves as a personal roadmap but also assists in coordinating with other parties involved, such as real estate agents, lenders, and attorneys. Regularly reviewing and updating this timeline is crucial in keeping the process on schedule and preventing any unforeseen delays. Additionally, a well-documented timeline can serve as a valuable reference for future transactions, offering insights and lessons learned that can streamline subsequent real estate endeavors.

Take Advantage of a Reverse Phone Lookup Tool

A reverse phone lookup tool can be a valuable asset in the real estate market, aiding both buyers and sellers. For buyers, it helps verify the identity of real estate agents, ensuring they are dealing with legitimate professionals. Sellers can use it to screen potential buyers, avoiding scams or fraudulent inquiries. Additionally, it allows both parties to gather more information about contacts, fostering trust and facilitating smoother transactions. By enhancing security and transparency, a reverse phone lookup tool contributes to a more efficient and secure home buying and selling process.

Store Documents Digitally

Embracing the shift toward digital document management is crucial in streamlining your home buying or selling process. The transition to digital formats, especially PDFs, enhances the organization and accessibility of your real estate documents. PDFs are renowned for their consistent formatting and compatibility across different devices and platforms.

Update Paperwork Promptly

The dynamic nature of real estate transactions means that changes can occur at any stage. It’s vital to keep all documents current. This includes promptly reflecting any amendments or updates in your paperwork. By maintaining up-to-date records, you minimize the risk of confusion or miscommunication later in the process, ensuring all parties are always informed of the latest developments. Regularly revisiting and revising documents also allows for a more responsive and adaptable approach to evolving transaction requirements.

Leverage Online Banking

Managing financial aspects efficiently is a cornerstone of a smooth home buying or selling experience. Online banking plays a pivotal role here, facilitating quick and secure financial transactions. Utilizing these services not only streamlines the handling of funds but also provides an organized digital trail. This digital record is particularly useful for tracking and referencing all transactions related to your property, aiding in both current and future financial management. Additionally, online banking often includes features that allow for easier budgeting and financial planning, enhancing your overall financial strategy.

Set Reminders to Stay on Top of Deadlines

In a process where timing is key, setting up reminders for important dates and deadlines is crucial. These reminders act as safeguards, ensuring you never miss critical steps such as inspection dates, mortgage approval deadlines, or closing appointments. By keeping these dates front and center, you can prepare and submit all necessary documents well in advance, avoiding last-minute rushes and potential hiccups in the process. Implementing these reminders can also help maintain a sense of calm and control, reducing stress and allowing for better focus on other important aspects of the transaction.

The real estate journey, while complex, can be made significantly smoother with meticulous organization and proactive strategies. A well-maintained timeline, digital document management, timely updates, online tools, and strategic reminders form a robust framework for success. These practices not only facilitate a seamless transaction but also instill confidence and clarity, allowing you to navigate the intricacies of real estate with assurance and efficiency. Ultimately, the mastery of these elements leads to a rewarding and stress-free property buying or selling experience.

Creating a home where grandparents, parents, and children live harmoniously under one roof requires thoughtful strategies. This arrangement can enrich lives, offering a unique blend of support, love, and shared experiences. Understanding and cooperation are paramount to thriving together.

Each generation brings its values, experiences, and expectations, making finding common ground and fostering mutual respect essential. Through open dialogue and flexibility, families can navigate the complexities of multigenerational living, turning potential challenges into opportunities for growth and deeper connections. CENTURY 21 Jordan-Link & Company shares more:

Unifying Through a Family Business

Starting a family business brings members closer, creating unity and a shared goal. An LLC offers benefits like limited liability and tax advantages, with less paperwork and flexibility. Families can start an LLC in California through ZenBusiness, avoiding lawyer fees and simplifying the process. It’s wise to read in-depth reviews before selecting a service, ensuring it meets your business needs.

Flexibility: The Foundation of Multigenerational Living

Accommodating everyone’s schedules and preferences is crucial in a household with different generations. Introducing flexible meal times and versatile shared spaces enables each family member to maintain their routines while contributing to the family’s rhythm. This approach minimizes conflicts over mundane issues, allowing for a smoother daily operation where everyone feels heard and accommodated.

Shared Responsibilities: A Tapestry of Teamwork

Engaging every family member in the household’s management distributes chores more equitably and instills a sense of ownership and belonging. Whether deciding on the week’s meals or setting cleaning schedules, involving everyone in these decisions fosters a team spirit. This collective approach encourages younger members to learn valuable life skills while giving older generations a continued sense of purpose and engagement.

Building Bridges Through Bonding Activities

Activities that cater to various interests and abilities are a fantastic way to strengthen family bonds. Whether it’s a weekly game night, storytelling sessions, or shared hobbies, these moments allow each generation to showcase their strengths and learn from one another. Such experiences are invaluable, fostering understanding, respect, and a deep sense of familial connection.

Cultivating a Unique Family Identity

Every family member’s contribution is vital to the household’s dynamics. Recognizing and valuing these contributions fosters a strong family identity, where individual achievements are celebrated as collective successes. This sense of unity and purpose strengthens the familial bond, providing a solid foundation for navigating life’s challenges together.

Fostering Open Communication

An environment where everyone feels comfortable expressing their feelings and needs is essential for harmony. Encouraging open and judgment-free dialogue aids in preempting misunderstandings and resolving conflicts efficiently. This culture of transparency ensures that all voices are heard and valued, promoting a healthier, more cohesive family dynamic.

Embracing Technology for Enhanced Connection

In today’s digital age, technology is a vital bridge between generations. Families can overcome the generational divide by integrating smart devices, online platforms, and educational tools into daily life.

This shared digital exploration fosters learning, entertainment, and communication, ensuring no member feels isolated or left behind. From grandparents learning to video calls to children exploring educational apps, technology becomes a shared language, bringing generations closer.

Respecting Privacy and Boundaries

Maintaining harmony in a multigenerational home necessitates a clear understanding and respect for personal boundaries. Establishing guidelines for privacy, such as designated quiet times or personal space rules, ensures every family member feels respected and valued. This balance between shared experiences and individual autonomy is crucial for sustaining a peaceful and cooperative environment.

Wrapping Up

Living in a multigenerational household offers a unique opportunity to foster deep, intergenerational relationships grounded in mutual respect, understanding, and shared experiences. Families can create a harmonious and supportive living environment by embracing flexibility, promoting teamwork, engaging in bonding activities, and maintaining open communication. This approach not only strengthens the familial bond but also enriches each member’s life, proving that together, we are stronger.

Understanding the Role of a CENTURY 21 Real Estate Agent in Marketing Your Property

When you decide to sell your house, finding the right real estate agent is crucial. An experienced CENTURY 21 agent doesn’t just list your home; they implement a strategic marketing plan designed to attract potential buyers and ensure your property stands out. Here’s a comprehensive guide on how CENTURY 21 agents help market your home and maximize its exposure.

Listing on the Multiple Listing Service (MLS)

One of the primary methods CENTURY 21 real estate agents use to market homes is by listing them on the Multiple Listing Service (MLS). This is a database of available properties that can be accessed by other agents and potential buyers.

Benefits of MLS Listing:

Increased Visibility: Your property gets maximum exposure to a wide audience.

Network of Agents: Other agents can bring their clients to view your home, increasing the chances of a quick sale.

Detailed Information: Listings include detailed descriptions, high-quality photos, and key property features, attracting more serious buyers.

Utilizing Yard Signs for Local Interest

A yard sign is a traditional yet effective marketing tool that captures the attention of passersby.

Advantages of Yard Signs:

Local Exposure: Neighbors might have friends or family looking to move into the area.

Immediate Contact Information: Potential buyers can quickly get your agent’s contact details.

Constant Advertisement: Your home is advertised 24/7 to anyone passing by.

Hosting Open Houses to Generate Buzz

Open houses are a great way to showcase your property to multiple potential buyers simultaneously.

Why Open Houses Work:

Creates Urgency: Seeing other interested buyers can prompt quick offers.

Convenient for Sellers: Multiple showings in a single day reduce the inconvenience.

Immediate Feedback: Agents can gather feedback from attendees to make necessary adjustments.

Showcasing on Agent’s Website for Professional Appeal

Having your property featured on your CENTURY 21 agent’s professional website ensures a polished presentation.

Benefits of Online Showcasing:

Professional Presentation: High-quality images and virtual tours can make your listing more appealing.

Targeted Audience: Visitors to the agent’s website are often serious buyers actively searching for properties.

SEO Optimization: Well-crafted listings can rank high on search engines, attracting more viewers.

Leveraging Social Media for Broad Reach

Social media platforms provide a vast audience for marketing your home.

Impact of Social Media Marketing:

Wide Audience Reach: Platforms like Facebook, Instagram, and Twitter have millions of users.

Shareable Content: Easy sharing options increase the chances of your listing being seen by more people.

Engagement and Interaction: Agents can interact with potential buyers, answer questions, and generate interest.

Providing Virtual Tours for Remote Buyers

Virtual tours have become an essential tool in real estate marketing, especially for out-of-town buyers.

Advantages of Virtual Tours:

Convenience: Buyers can view your home anytime, from anywhere.

Detailed Viewing: 3D tours allow buyers to explore the property in detail.

Technological Edge: Shows that your agent is using the latest marketing tools.

Creating a Comprehensive Marketing Plan

A successful real estate marketing strategy involves a combination of methods tailored to attract the right buyers.

Components of a Robust Marketing Plan:

Professional Photography: High-quality images that highlight the best features of your home.

Engaging Descriptions: Compelling and accurate descriptions that appeal to buyers.

Targeted Advertising: Utilizing both online and offline channels to reach a broad audience.

Regular Updates: Keeping the listing information current and making necessary adjustments based on feedback.

Conclusion: Partner with a Professional CENTURY 21 Real Estate Agent

Working with a professional CENTURY 21 real estate agent offers numerous benefits when it comes to marketing your home. They bring a wealth of experience, utilize a variety of tools, and implement strategies that ensure maximum exposure for your property. If you’re ready to sell, choose a CENTURY 21 agent who will craft a comprehensive marketing plan tailored to your needs.

By leveraging these methods, you can rest assured that your home will receive the attention it deserves, ultimately leading to a successful sale. Whether you’re working with a local realtor or a national expert, CENTURY 21 agents are equipped to handle all your marketing needs effectively.

Certainly! Here are several external links relevant to the topics covered in the article:

Selling a house can be a complex process, but with the right guidance, it can be smooth and rewarding. Century 21 Jordan-Link & Co. is here to answer all your questions and ensure you get the best deal possible.

How Do I Determine the Right Price for My House?

Setting the right price is crucial. Our professional realtors will conduct a comparative market analysis to evaluate your home’s value. This helps in pricing your property competitively, attracting serious buyers, and ensuring you get the best return on your investment.

What Should I Do to Prepare My House for Sale?

First impressions matter. Our team advises on essential repairs, decluttering, and staging to make your home more appealing. Simple updates can significantly enhance your home’s marketability and value.

How Will You Market My Property?

Century 21 Jordan-Link & Co. uses a comprehensive marketing strategy that includes online listings, social media promotion, and traditional advertising. We target potential buyers through various channels to maximize exposure.

What Are the Costs Involved in Selling a House?

Selling a house involves several costs, including agent commissions, closing fees, and potential repairs. Our realtors will provide a detailed breakdown of these expenses, so you know what to expect.

How Long Will It Take to Sell My House?

The time it takes to sell a house varies based on market conditions, location, and pricing. Our experienced agents will give you a realistic timeline and work diligently to close the deal as quickly as possible.

Can I Sell My House If I Still Have a Mortgage?

Yes, you can sell your house with an existing mortgage. The proceeds from the sale will typically be used to pay off the mortgage balance. Our team will guide you through this process to ensure a smooth transaction.

Why Should I Choose Century 21 Jordan-Link & Co.?

Our professional realtors have extensive knowledge and experience in the real estate market. We offer personalized service, strategic marketing, and expert negotiation skills to help you achieve the best outcome. Learn more about our team and our services.

For any other questions, feel free to contact us. We’re here to help you every step of the way.

Navigating the housing market can be a daunting task, especially with the ever-changing landscape of home prices and mortgage rates. Whether you’re a first-time homebuyer, a homeowner looking to upgrade, or someone considering selling, understanding the factors influencing these critical aspects is essential. In this article, we’ll delve into the current state of the housing market, explore the various factors affecting home prices and mortgage rates, and provide insights and predictions for the future.

Current State of the Housing Market

Overview of Recent Trends

The housing market has seen significant fluctuations over the past few years, largely influenced by the COVID-19 pandemic. Home prices surged as demand outstripped supply, driven by low mortgage rates and a desire for more spacious living environments. However, as we move into 2024, the market dynamics are beginning to shift.

Impact of the Pandemic on Home Prices

The pandemic brought about a unique set of challenges and opportunities in the housing market. Initially, there was a rush to buy homes, spurred by historically low mortgage rates and the need for home offices. This demand pushed home prices to record highs. As the economy stabilizes, we are seeing a normalization in home price growth.

Factors Influencing Home Prices

Economic Indicators

Economic health is a primary driver of home prices. Factors such as inflation rates, employment levels, and GDP growth play significant roles.

Inflation Rates

Inflation impacts everything from the cost of groceries to the price of homes. When inflation rises, the purchasing power of money decreases, often leading to higher home prices as sellers try to maintain their profit margins.

Employment Rates

A robust employment market means more people have the financial stability to buy homes, increasing demand and driving up prices. Conversely, high unemployment can suppress demand and stabilize or even lower home prices.

GDP Growth

The Gross Domestic Product (GDP) is a measure of the overall economic activity. Strong GDP growth usually correlates with a healthy housing market, as economic prosperity encourages home buying.

Supply and Demand Dynamics

The balance between housing supply and demand is a critical determinant of home prices.

Housing Supply Shortages

A shortage of available homes can drive prices up as buyers compete for limited inventory. This shortage can be due to various factors, including zoning laws, construction delays, and natural disasters.

Population Growth and Housing Demand

Areas with rapid population growth often see increased demand for housing. As more people move into these regions, the competition for homes intensifies, pushing prices higher.

Building Permits and New Construction

The rate at which new homes are built also affects supply. An increase in building permits and new construction can help alleviate supply shortages and moderate price growth.

Interest Rates and Mortgage Rates

Current Mortgage Rates

Mortgage rates have a direct impact on home affordability. Over the past year, rates have fluctuated, influenced by Federal Reserve policies and broader economic conditions.

Historical Trends in Interest Rates

Looking at historical trends can provide context for current rates. Historically, mortgage rates have varied widely, influenced by inflation, economic policies, and global financial events.

Federal Reserve Policies

The Federal Reserve’s monetary policies, including interest rate adjustments, play a crucial role in determining mortgage rates. When the Fed raises interest rates to combat inflation, mortgage rates typically follow suit.

Predictions for Home Prices

Expert Opinions on Future Home Prices

Experts are divided on the future of home prices. Some predict continued growth, albeit at a slower pace, while others foresee a slight correction as the market balances itself.

Regional Variations in Home Price Predictions

Home price trends can vary significantly by region. Areas with strong economic growth and high demand may continue to see price increases, while others might experience stabilization or slight declines.

Predictions for Mortgage Rates

Forecasts from Financial Institutions

Financial institutions provide various forecasts for future mortgage rates. Most agree that rates will likely rise modestly as the economy continues to recover.

Factors Affecting Future Mortgage Rates

Several factors will influence future mortgage rates, including inflation, Federal Reserve policies, and the overall economic outlook.

Impact on Homebuyers and Sellers

Advice for First-Time Homebuyers

First-time homebuyers should focus on financial preparedness, understanding market conditions, and working with experienced real estate agents to navigate the complexities of the market.

Strategies for Current Homeowners

Current homeowners considering selling should stay informed about market trends, invest in home improvements, and work with professionals to maximize their home’s value.

Tips for Navigating the Market

Understanding Market Trends

Staying informed about market trends is crucial. Regularly reading market reports and news can provide valuable insights into the best times to buy or sell.

Working with Real Estate Agents

A knowledgeable real estate agent can be an invaluable asset. They can provide expert advice, market insights, and negotiation support to help you achieve your real estate goals.

Mortgage Options and Financial Planning

Understanding your mortgage options and having a solid financial plan are essential. Explore different loan types, interest rates, and repayment plans to find the best fit for your situation.

The Role of Government Policies

Housing Policies and Regulations

Government policies and regulations can significantly impact the housing market. Policies aimed at increasing housing supply, providing buyer assistance, and regulating mortgage lending all play a role.

Government Programs and Assistance

Various government programs are available to assist homebuyers, particularly first-time buyers. These programs can provide financial assistance, lower interest rates, and other benefits.

Conclusion

The future of home prices and mortgage rates is shaped by a complex interplay of economic indicators, supply and demand dynamics, and government policies. While predicting exact trends can be challenging, staying informed and working with professionals can help you navigate the market successfully.

Why Choose Century 21 Jordan-Link & Co. for Luxury Homes?

Looking for luxury homes near you? Century 21 Jordan-Link & Co. offers unmatched expertise and personalized services to help you find your dream home. Our professional realtors specialize in the luxury market, ensuring a seamless buying or selling experience.

Expert Realtors for Premium Properties

Our team of seasoned realtors understands the intricacies of the luxury home market. With extensive knowledge and experience, we provide valuable insights and strategic advice to help you make informed decisions. Whether buying or selling, we ensure your transaction is smooth and stress-free.

Personalized Services for Discerning Clients

At Century 21 Jordan-Link & Co., we offer personalized services tailored to your unique needs. Our commitment to excellence means we go above and beyond to meet your expectations. From property tours to negotiation, we handle every detail with precision and care.

Seamless Transactions with Professional Guidance

Navigating the luxury real estate market can be challenging, but our professional guidance ensures a seamless process. We manage all aspects of your transaction, providing clear communication and expert advice. Trust Century 21 Jordan-Link & Co. to handle your luxury home needs with the utmost professionalism.

Contact Us Today

Ready to find your dream luxury home near you? Contact us today to schedule a consultation with one of our expert realtors. Visit our Contact Us page for more information. Learn more about our team and services on our About Us page. Interested in joining our team? Check out our Join C21 page for career opportunities.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

")